Introduction: The Paradox of Diaspora Wealth!

At first glance, life in the UK looks like financial success.

Steady income. Strong currency. Better opportunities.

But beneath the surface, a different reality is unfolding.

Many Kenyans in the UK are not struggling because they earn too little—

they are struggling because too much of what they earn is already committed.

This is not just opinion. It is backed by research, policy reports, and real-life diaspora experiences.

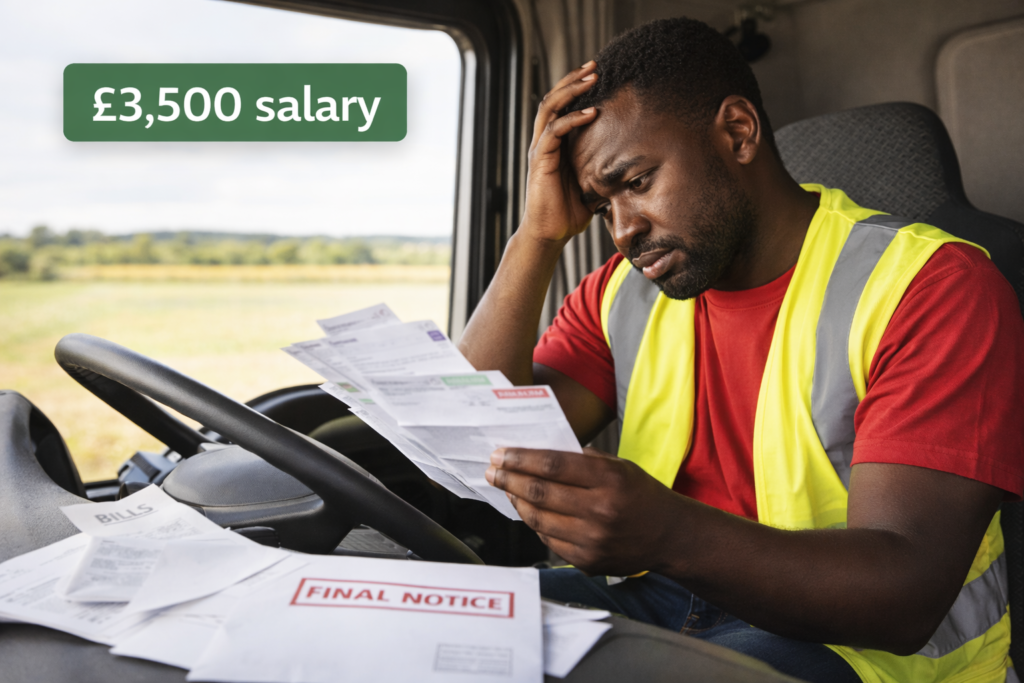

1. Income Without Margin: Working, But Still Struggling!

According to the Joseph Rowntree Foundation, 3.8 million workers in the UK are living in poverty, and the in-work poverty rate stands at 12%.

This tells us something important: Having a job in the UK no longer guarantees financial stability. That matters for the Kenyan diaspora because many migrants are concentrated in sectors or work patterns where pay is steady but not wealth-building: shift work, care, transport, hospitality, agency work, and part-time or insecure roles. JRF notes that Black African and Caribbean individuals are three times more likely than the average worker to be employed through agencies, and earlier analysis found a 22 pence per hour pay penalty associated with agency employment.

For many Kenyans in the diaspora:

- Work is consistent,

- Income is predictable,

- But savings are minimal.

Why?

Because income is being stretched across multiple obligations, before it can build wealth.

2. Housing: The Silent Wealth Killer

According to the Resolution Foundation, ethnic minority households in the UK spend a higher proportion of their income on housing compared to White British households.

At the same time, data from the UK Government Ethnicity Facts and Figures shows:

- 70% of White British households own homes.

- Only 22% of Black African households do.

This is critical.

Rent is not just an expense, it is money that does not convert into wealth.

So even when a Kenyan professional earns well:

- £1,200–£2,000+ may go to rent.

- Nothing is building equity.

So a Kenyan nurse, bus driver, support worker, or warehouse employee may earn regularly every month, but if a large share goes to rent in London, Birmingham, Luton, Manchester, or other high-cost areas, that income may never convert into equity. That is how someone can be working hard and still remain “broke” in a long-term sense.

Result: Years of work… but little long-term financial progress.

3. The Hidden Cost of Staying Legal

According to the UK Parliament House of Commons Library:

- Immigration Health Surcharge: £1,035 per year,

- Visa pathways can cost £5,000–£10,000+.

A report by The Guardian describes migrants as effectively “paying twice”:he House of Commons Library says an immigration health surcharge of £1,035 per year applies to many visa holders, and that sponsoring a five-year work visa can cost around £10,000 for a small business, while a two-and-a-half-year spouse or partner visa can cost around £5,000.

This is a major financial drain.

Instead of saving for; Deposits, Investments and for Business, many migrants are funding their right to remain in the UK.

4. The “Black Tax”: Supporting Two Economies at Once!

This is where the reality hits hardest.

According to The Guardian, many African diaspora workers face what is commonly referred to as the “black tax”, the expectation to financially support extended family back home. The UK has become a major remittance source for Kenya. Business Daily, citing CBK data, reported that in 2025 the UK overtook Saudi Arabia as Kenya’s second-largest remittance source, with UK inflows at $360.2 million.

A Kenyan in the UK, Anthony Kimere, shared:

“You feel obligated to give back because you know the situation.”

And the reality?

- School fees,

- Medical bills,

- Rent support,

- Emergencies.

According to Kenya’s State Department for Diaspora Affairs, 80% of remittances are used for consumption, not investment.

That means most diaspora money is solving today’s problems, not building tomorrow’s wealth.

5. The Cost of Sending Money (And Losing It Quietly).

According to the Migration Observatory at Oxford University: Sending money from the UK costs around 4.8%–6% per transaction.

That may sound small. But over time:

- Monthly remittances,

- FX spreads.

- Transfer fees.

Become a consistent wealth leak. For someone sending £500 monthly, you could lose hundreds of pounds annually, without noticing

6. Living Between Two Cost-of-Living Crises!

According to the Office for National Statistics 62% of UK adults report increased cost of living.

But diaspora communities face a unique challenge:

They are affected by inflation in two countries at once;

- UK bills are rising; ONS data for late 2025 showed that 62% of adults in Great Britain said their cost of living had increased compared with a month earlier, and cost of living remained one of the top concerns nationally.

- Kenya needs more support: Witness accounts and long-running diaspora reporting point to a social illusion: people back home often see the UK salary, the travel, the phone, the photos, or the pounds, but they do not see the rent, council tax, transport, visa renewals, childcare, agency gaps, or remittance obligations. The result is inflated expectations from relatives and sometimes status pressure on the migrant.

As one diaspora sender put it (via The Guardian):

They feel “pulled from both sides.”

7. The Bigger Problem: Income Is Not Turning Into Wealth;

According to the London School of Economics:

- The ethnic wealth gap in the UK is widening.

- Black African households hold significantly lower accumulated wealth.

This is the key distinction:

- Many Kenyans are earning.

- But fewer are building assets.

Final Analysis: So, Are Kenyans in the UK Broke?

The statement:

“Most Kenyans in the UK are broke”

- Too simplistic.

- Not fully supported by data.

But this is true:

Many are financially stretched—not because they earn little, but because their income is split across survival, obligation, and structural barriers.

Golden Tai Africa Insight: The Real Problem Is Not Income—It’s Structure!

If you want to understand diaspora finance, understand this:

- The issue is not how much you earn.

- The issue is how much you keep, grow, and protect.

What Needs to Change (Diaspora Playbook):

- Shift from consumption to investment.

- Track real cost of remittances (fees + FX).

- Prioritise asset building (property, MMFs, pensions).

- Set boundaries on financial obligations.

Closing Thought:

You can earn in pounds…

But if your system is broken, you will still live under pressure.

Wealth is not built by income alone—it is built by control.

Leave a Reply