A Shift Toward Digital Tax Enforcement, Crypto Oversight and Import Taxes:

The Finance Bill 2026 marks another major evolution in Kenya’s taxation landscape. But unlike the explosive public reaction that greeted the Finance Bill 2024, this year’s proposals are more targeted, technical and compliance-driven.

At its core, the Bill seeks to widen the tax base, strengthen Kenya Revenue Authority (KRA) enforcement powers, tighten oversight over the digital economy, and raise revenue from imports, gambling and emerging technologies such as cryptocurrency. At the same time, the government is proposing selective incentives for manufacturing, infrastructure and strategic sectors.

What stands out is not necessarily the introduction of many entirely new taxes, but rather the government’s growing determination to ensure that previously under-monitored sectors are now fully visible within the tax system.

Mobile Phones Face Proposed 25% Excise Duty:

One of the most noticeable proposals is the introduction of a 25% excise duty on telephones for cellular networks and wireless systems.

Under the current framework, imported phones already attract:

- Import duty.

- VAT.

- Import declaration fees.

- Railway development levy.

The proposed amendment adds another significant excise layer.

Existing Position;

Previously, imported mobile phones were not subjected to this proposed 25% excise duty category in the manner now being proposed.

Proposed Change;

The Bill now introduces:

- a direct excise duty structure on cellular phones;

- broader taxation around telecom-related imports and devices.

Likely Impact:

If passed in its current form:

- smartphone prices may rise;

- internet accessibility costs could increase;

- the cost of digital inclusion may become higher, especially for low-income users.

This could particularly affect Kenya’s youth driven digital economy, where smartphones are now essential for:

- banking,

- e-commerce,

- online jobs,

- education,

- and content creation.

Kenya Moves Closer to Full Crypto Regulation:

Perhaps the most globally significant proposal in the Bill is the introduction of detailed reporting obligations for virtual asset service providers.

Existing Position;

Kenya has historically had an uncertain and fragmented approach toward cryptocurrency. While the Central Bank of Kenya repeatedly warned against crypto use, the country lacked a comprehensive taxation and reporting structure for digital assets.

Proposed Amendment;

The Finance Bill 2026 now requires virtual asset providers to:

- file information returns;

- identify reportable users;

- maintain transaction records;

- support exchange of tax information with foreign jurisdictions.

Why This Matters

Kenya is effectively aligning itself with global trends already seen in:

- the United Kingdom,

- the European Union,

- the United States,

- and OECD member countries.

The government’s objective appears clear:

crypto should no longer exist outside formal tax visibility.

This is likely to affect:

- crypto exchanges,

- digital asset marketplaces,

- token trading platforms,

- and fintech firms dealing with virtual assets.

For Kenya’s growing tech ecosystem, this could bring both:

- greater legitimacy,

- and heavier compliance obligations.

Betting and Gambling Come Under Tighter Tax Control:

The Finance Bill 2026 also intensifies oversight over betting and gambling activities.

Existing Position;

Kenya already taxes betting through:

- excise duty,

- withholding tax on winnings,

- and betting taxes on operators.

However, loopholes and ambiguities have persisted around:

- withdrawals,

- wallet balances,

- and the treatment of winnings.

Proposed Amendment;

The Bill introduces clearer legal definitions for:

- “withdrawals”;

- “winnings”;

- betting wallet transactions.

Likely Outcome

The proposed changes strengthen KRA’s ability to:

- track betting activity,

- tax gambling payouts more efficiently,

- and reduce tax leakages in online betting ecosystems.

For the betting industry, compliance costs are likely to rise further.

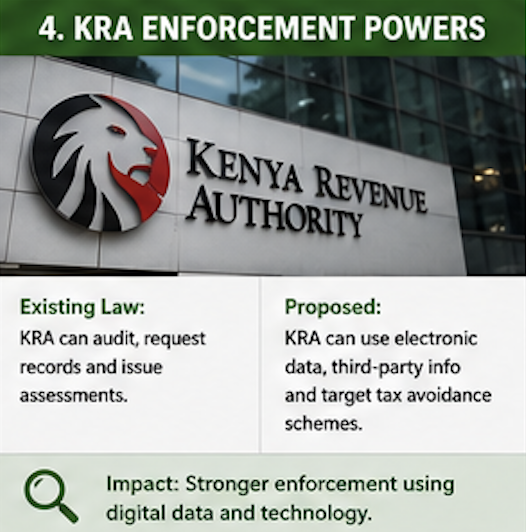

KRA Gains Stronger Digital Enforcement Powers:

One of the biggest structural themes in the Bill is expanded enforcement authority for KRA.

Existing Position;

KRA already has powers to:

- audit taxpayers,

- request records,

- issue assessments,

- and investigate tax evasion.

Proposed Change;

The Finance Bill broadens KRA’s ability to rely on:

- electronic records,

- digital systems,

- third-party information,

- automated data systems,

- and anti-tax avoidance provisions.

What This Means

Kenya is steadily moving toward a data-driven tax administration system.

Businesses operating informally while relying heavily on:

- digital payments,

- fintech systems,

- online marketplaces,

- or platform economies

may increasingly find themselves within KRA’s visibility range.

The Bill also introduces provisions targeting “tax avoidance schemes,” giving KRA stronger legal footing to challenge arrangements designed mainly to reduce taxes artificially.

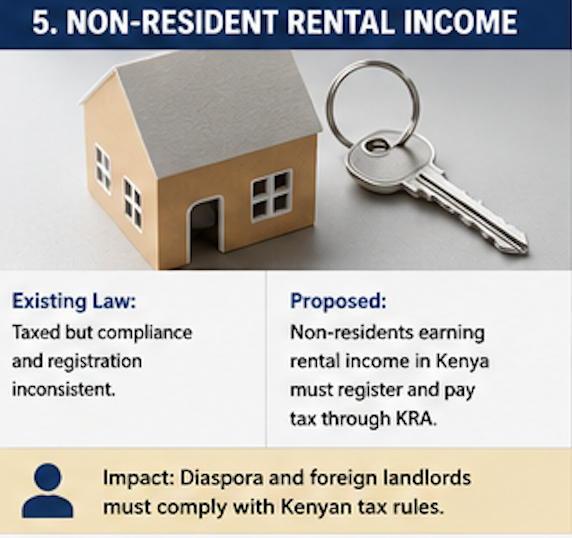

Foreign Property Owners in Kenya Targeted:

The Bill introduces a proposed non-resident rental income tax framework.

Existing Position;

Taxation of foreign landlords in Kenya has existed in practice, but enforcement and registration compliance have remained inconsistent.

Proposed Amendment;

The Bill formalizes a simplified framework requiring non-resident persons earning rental income in Kenya to:

- register for tax,

- account for rental income tax,

- and comply through KRA systems.

Likely Impact

This may significantly affect:

- diaspora investors,

- offshore property owners,

- foreign-owned rental developments.

Kenya appears determined to ensure that locally generated property income is taxed regardless of where the owner resides.

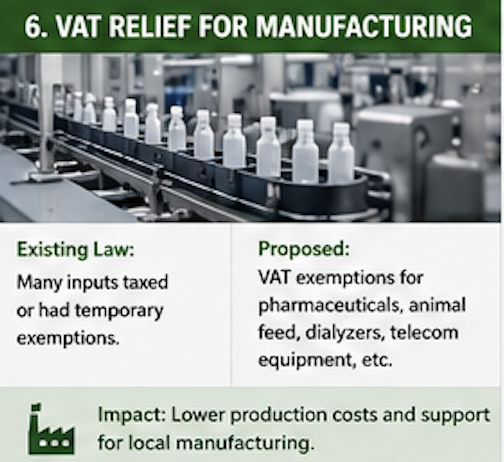

Selected Manufacturing Sectors Receive Tax Relief:

While the Bill increases taxation in some areas, it also introduces targeted VAT exemptions and incentives.

Beneficiaries Include:

- pharmaceutical manufacturing;

- animal feed production;

- sugar industry logistics;

- medical equipment such as dialyzers;

- certain telecom infrastructure projects.

Existing Position;

Some of these sectors either faced full VAT exposure or operated under temporary exemptions.

Proposed Change:

The government is now expanding or restructuring exemptions for strategic sectors considered important for:

- healthcare,

- food security,

- telecommunications,

- and industrialization.

This aligns with Kenya’s broader manufacturing and local production ambitions under industrial growth strategies.

Infrastructure and PPP Projects Receive Support:

The Bill also introduces VAT-related support measures for approved Public Private Partnership (PPP) infrastructure projects.

Existing Position;

PPP investors often complained about high upfront tax costs on infrastructure implementation.

Proposed Amendment;

Certain supplies and services used directly in approved infrastructure projects may now qualify for tax relief.

Why This Matters

Kenya is signaling continued reliance on:

- private infrastructure financing,

- large-scale development partnerships,

- and foreign capital participation.

This could benefit:

- transport projects,

- energy infrastructure,

- telecommunications expansion,

- and public works developments.

Tobacco, Plastics and Imports Face Heavier Taxation:

The Bill proposes multiple excise adjustments affecting:

- cigarettes,

- tobacco substitutes,

- plastics,

- ceramics,

- packaging materials,

- and selected imported products.

Existing Position;

Many of these goods were already taxed, but under lower or differently structured rates.

Proposed Amendment;

The Bill either:

- increases rates,

- restructures categories,

- or removes favorable wording that previously reduced tax exposure.

Likely Effect

Consumers could eventually face:

- higher retail prices,

- increased packaging costs,

- and more expensive imported goods.

Road Maintenance Levy Slightly Reduced:

In a rare relief measure, the Bill proposes reducing part of the Road Maintenance Levy contribution from KSh 3 to KSh 1.50.

However, the actual effect on fuel prices may be modest once other taxes and global oil prices are considered.

Conclusion: Kenya’s Tax System Is Becoming More Digital, More Aggressive and More Global:

The Finance Bill 2026 reflects a government increasingly focused on:

- closing tax loopholes,

- digitizing enforcement,

- expanding taxation into emerging sectors,

- and improving compliance visibility.

Compared to previous years, the Bill is less politically explosive but far more technically transformative.

Its strongest focus areas are now clear:

- digital transactions,

- crypto assets,

- gambling,

- imports,

- multinational reporting,

- and data-driven tax administration.

At the same time, the government is attempting to balance this with selective support for:

- manufacturing,

- healthcare,

- infrastructure,

- and strategic industrial sectors.

Whether these measures ultimately stimulate growth or increase the cost of doing business will depend heavily on:

- final parliamentary amendments,

- implementation,

- and the broader economic environment in Kenya over the next few years.

************************************************************************

What is your take on this proposed measures? Do they meet your expectations?

Leave a Reply