The Big Picture!

Lifestyle inflation, also known as lifestyle creep, is emerging as one of the most subtle but damaging threats to wealth creation in the United Kingdom in 2026.

While headline inflation has eased to around 3.0%, and wages have begun to show modest real growth, many households are not experiencing meaningful financial progress. Instead, increased earnings are being absorbed into higher living standards, expanded consumption, and recurring financial commitments.

The result is a “wealth stagnation trap”: incomes are rising, but net worth is not.

1. Understanding Lifestyle Inflation in the UK Context.

Lifestyle inflation is not driven by necessity, but by behavioural adjustment.

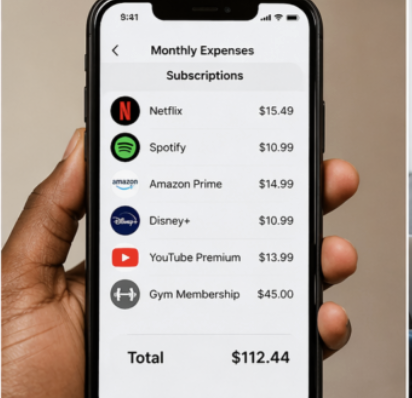

As income rises, spending increases in ways that feel justified:

- Upgrading housing or location.

- Increasing convenience spending (deliveries, subscriptions).

- Financing better cars, phones, or holidays.

- Expanding “comfort” expenses that become permanent.

Unlike CPI inflation, which is external, lifestyle inflation is internal and often invisible.

In the UK’s current economic phase, post cost-of-living crisis, this is particularly dangerous because it is disguised as recovery.

2. The UK Economic Backdrop (2026 Reality Check)

Recent data from the Office for National Statistics confirms a fragile but improving environment:

- Inflation (CPI): ~3.0% (early 2026).

- Nominal wage growth: ~3.8%.

- Real wage growth: ~0.4%.

- Average weekly earnings: ~£690.

At the same time:

- Average household spending: ~£623/week.

- Housing, fuel & power: ~18% of total spend.

- Transport: ~14%.

This tells a clear story:

Households have slightly more breathing room, but not enough to absorb poor financial decisions.

*CPI – Consumer Price Index.

3. The Three Drivers of Lifestyle Inflation in the UK.

3.1 The “Recovery Spending” Effect

After years of restriction (2022–2024), households are naturally reverting to comfort spending:

- Dining out.

- Travel and short breaks.

- Premium subscriptions.

- Lifestyle upgrades.

This is not reckless, it is psychological.

But it delays financial rebuilding.

3.2 The Mortgage Reset Pressure

According to UK Finance:

- 1.6 million mortgages reset in 2025

- 1.8 million expected to reset in 2026

The impact is severe.

A typical mortgage shift illustrates the pressure:

- £200,000 mortgage at 2% → ~£848/month.

- Same mortgage at 5% → ~£1,169/month.

That is an increase of over £300/month.

For households that allowed lifestyle costs to expand beforehand, this creates an immediate financial squeeze, often eliminating savings capacity entirely.

3.3 Digital & Frictionless Spending.

The rise of seamless consumption is accelerating lifestyle inflation:

- Buy Now Pay Later (BNPL) usage: ~1 in 5 UK adults

- Among ages 25–34: ~30% usage.

- Major use cases:

- Lifestyle purchases.

- “Treat spending”.

- Fashion and beauty.

Platforms like Klarna reduce the psychological pain of spending, allowing consumption to rise faster than income awareness.

4. The Real Risk: Wealth Stagnation, Not Poverty

Contrary to popular belief, the biggest danger is not immediate financial collapse.

It is long-term stagnation.

Data shows:

- UK household saving ratio: ~9.9% (Q4 2025)

- Yet:

- 10% of adults have no savings.

- 21% have less than £1,000.

- 24% show low financial resilience.

This creates a dangerous illusion:

Households appear stable—but remain financially fragile.

5. The Mechanics of Wealth Erosion.

5.1 Commitment Creep

Wealth is not lost in large decisions, it leaks through:

- Subscriptions.

- Finance agreements.

- Incremental lifestyle upgrades.

These become fixed monthly obligations.

5.2 The Opportunity Cost Effect

Every £100 absorbed into lifestyle is £100 not invested.

Over time, this compounds significantly.

At modest returns, small monthly leaks translate into tens of thousands in lost wealth over decades.

5.3 The Reclassification Trap

What was once a luxury becomes perceived as a necessity:

- High-speed internet.

- Premium groceries.

- Ride-hailing convenience.

- Subscription ecosystems.

This shifts the baseline cost of living upward permanently.

6. Real-Life UK Scenarios.

Case 1: The Salary Illusion

A professional earns £3,000/month and receives a £300 pay rise.

Instead of saving:

- £120 → car upgrade.

- £80 → subscriptions & services.

- £100 → lifestyle upgrades.

Result: No improvement in net worth.

Case 2: The Mortgage Shock

A household maintains spending habits from low-rate years.

Mortgage resets → +£300/month

Outcome:

- Savings disappear.

- Credit usage increases.

Case 3: The Digital Consumer

A young professional uses BNPL regularly:

- £50 here, £80 there.

- No immediate pain.

Result: Income feels sufficient, but cash flow is constantly constrained.

7. Strategic Conclusion

The UK is not in a false recovery, it is in a fragile recovery phase.

Lifestyle inflation is not destroying wealth instantly.

It is preventing wealth from forming.

The real issue is not overspending.

It is the failure to convert rising income into assets.

8. Recommendations: How to Defeat Lifestyle Inflation

1. Automate Wealth First

Increase savings immediately after any pay rise.

2. Maintain Spending Discipline

Apply structured rules such as:

- 50% Needs

- 30% Wants

- 20% Savings/Investment

3. Build Financial Resilience

Follow guidance from MoneyHelper:

- Target 3–6 months of emergency savings

4. Introduce Friction into Spending

- Remove saved cards

- Limit BNPL usage

- Audit subscriptions annually

5. Prioritise Asset Growth

Use available tools:

- ISAs (up to £20,000 annually)

- Pensions (SIPP/workplace contributions)

Final Verdict

Lifestyle inflation in the UK is not loud.

It does not announce itself in financial crises.

It operates quietly,through comfort, convenience, and gradual upgrades.

And that is precisely why it is dangerous.

You do not notice it when it starts.

But you feel it when wealth fails to grow.

Leave a Reply