The psychology of money in African households cannot be understood through a purely Western lens of individualism, retirement planning, and personal wealth accumulation. Instead, it is shaped by a deeply rooted blend of communal responsibility, historical experience, economic volatility, and cultural identity. Money, in many African contexts, is not just a financial tool, it is a social instrument, a survival mechanism, and a symbol of dignity.

This creates a financial mindset that is both resilient and complex, often balancing competing priorities that are rarely present in more individualistic societies.

1. Money as a Communal Resource, Not a Private Asset.

In many African households, money is not viewed as belonging solely to the individual who earns it. Instead, it is seen as a shared resource, tied to the wellbeing of the extended family.

A young professional in Nairobi, Lagos, or even in the diaspora (London, Manchester, Birmingham) is rarely just earning for themselves. Their income is often expected to support:

- Parents and siblings,

- Extended relatives,

- School fees for younger family members,

- Medical emergencies back home.

This communal approach is rooted in Ubuntu philosophy, “I am because we are.” Financial success, therefore, carries moral obligations.

While this builds strong family safety nets, it also creates pressure and delayed personal wealth accumulation. Saving for a house deposit in the UK, for example, can feel secondary to paying hospital bills back home.

2. The Reality of “Black Tax”.

Closely tied to communalism is the concept of “black tax” the informal but deeply felt obligation to financially support extended family.

Unlike formal taxation, this is:

- Unstructured,

- Emotionally driven, and

- Non-negotiable in many cases.

For many Africans, especially first-generation migrants, this means:

- A portion of income is already “spoken for” before it arrives,

- Financial planning must accommodate unpredictable requests,

- Personal financial goals (investments, savings) are often postponed.

This creates a psychological tension between:

- Self-progress,

- Family responsibility.

It is not uncommon to find someone earning a good salary but feeling financially stuck, not because of poor discipline, but because of distributed financial obligations.

3. Survival Mindset vs. Wealth-Building Mindset.

Many African economies have historically experienced:

- Currency volatility,

- Inflation spikes,

- Political uncertainty,

- Limited social safety nets.

This shapes a survival-first mentality around money.

Instead of asking:

“How do I grow wealth over 30 years?”

The question often becomes:

“How do I remain financially stable this year?”

This leads to two contrasting behaviours:

a) Extreme Caution

- Avoidance of financial risk,

- Preference for saving rather than investing,

- Fear of losing hard-earned money.

b) High-Risk Hustling

- Multiple side hustles,

- Informal business ventures,

- Quick-return investments.

This duality explains why you may find someone who is both:

- Very conservative with savings.

- Yet willing to take bold risks in business.

It is not contradiction, it is adaptation.

4. The Side Hustle Culture.

In many African households, relying on a single income stream is seen as dangerous.

This has led to a widespread culture of side hustles, where individuals:

- Run small businesses alongside employment,

- Trade goods (locally or across borders),

- Invest in informal ventures.

The psychology behind this is simple:

“Never depend on one source of income.”

This mindset is increasingly visible even among Africans in the diaspora. A nurse in the UK may also:

- Sell products online,

- Invest in land back home,

- Participate in group savings schemes.

Side hustles are not just about ambition, they are about security and control.

5. Preference for Tangible Assets.

Another defining feature is the strong preference for visible, tangible assets such as:

- Land,

- Houses,

- Livestock.

These are often valued more than:

- Stocks,

- Bonds,

- Pension funds.

Why?

Because tangible assets provide:

- Security (they cannot “disappear” like money in unstable systems),

- Status (visible proof of success),

- Legacy (something to pass down to future generations).

However, this can sometimes lead to:

- Low liquidity (cash flow constraints),

- Underinvestment in financial markets,

- Difficulty responding to emergencies.

This creates a paradox:

Asset-rich, cash-poor households.

6. Generational Money Trauma.

Financial behaviours in African households are often shaped by stories passed down through generations.

These stories may include:

- Periods of extreme poverty,

- Loss of wealth due to political instability,

- Economic crises or displacement.

As a result, money is often associated with:

- Fear,

- Urgency,

- Survival.

This creates what can be described as “money trauma”, influencing:

- Risk tolerance,

- Spending habits,

- Saving behaviour.

For example:

- A parent who experienced scarcity may discourage investment risk.

- A child may grow up overly cautious or, conversely, overly aggressive financially.

Money, therefore, carries emotional weight, not just numerical value.

7. Social Status and the “Man in the Car Paradox”.

In many African societies, wealth is not only accumulated, it is also displayed.

Visible success brings:

- Respect,

- Social standing,

- Family pride.

This can lead to what is often called:

The “man in the car paradox”

Where individuals:

- Invest in visible assets (cars, events, lifestyle),

- While neglecting long-term wealth-building.

This is not purely vanity, it is cultural signaling.

Owning a car, building a home, or hosting a large event communicates:

“I have succeeded. My family is secure.”

However, it can also create financial strain when image outpaces reality.

8. Informal Financial Systems and Discipline.

Despite limited access to formal financial education, African households often demonstrate strong financial discipline through informal systems such as:

- Rotating savings groups (e.g., chama, stokvel),

- Community lending circles,

- Peer accountability systems.

These systems:

- Encourage consistent saving,

- Provide access to lump sums,

- Build financial habits.

They are based on trust and social pressure, rather than contracts and institutions.

In many cases, they are more effective at enforcing discipline than formal banking systems.

9. The Evolving Role of Women.

Traditionally, financial control in many African households was male-dominated. However, this is rapidly changing.

Women are increasingly:

- Income earners,

- Investors,

- Financial decision-makers.

This shift is redefining the psychology of money by:

- Prioritizing stability and long-term planning,

- Investing in education and family wellbeing and

- Building independent wealth.

In many households today, women are the financial anchors, quietly driving economic transformation.

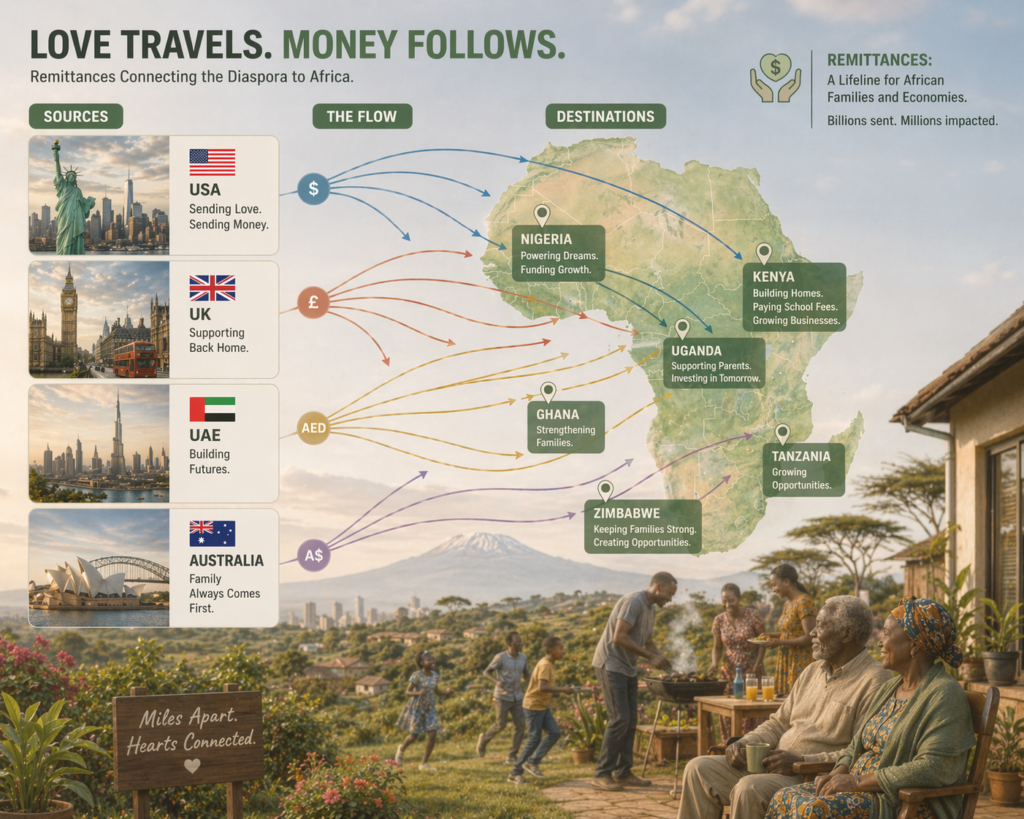

10. Diaspora Dynamics: Between Two Worlds.

Africans living abroad, especially in places like the UK, USA, Middle East and Europe, experience a unique financial psychology:

They operate between:

- A Western financial system (structured, individualistic),

- An African expectation system (communal, relational).

This creates:

- Dual financial obligations.

- Currency conversion pressures.

- Emotional strain.

A salary in pounds may look strong on paper, but once:

- Rent is paid.

- Remittances are sent.

- Family obligations are met.

The reality can feel very different.

Conclusion: A System Built on Responsibility and Resilience.

The psychology of money in African households is not flawed, it is contextual.

It reflects:

- A history of resilience.

- A culture of shared responsibility.

- A need to adapt to uncertainty.

However, it also presents challenges:

- Delayed wealth accumulation.

- Financial pressure.

- Limited investment diversification.

The opportunity going forward lies in balancing both worlds:

- Maintaining communal values.

- While embracing structured wealth-building.

As one Swahili saying goes:

“Haba na haba hujaza kibaba” — little by little fills the measure.

For African households, the future of wealth will not come from abandoning their values, but from refining them, building systems where community support and personal prosperity can grow side by side.

Leave a Reply